Briefing · Semiconductors

NVIDIA's SEC Filing Anchors Data Center AI Demand Narrative Around Hopper and Ethernet Infrastructure

NVIDIA's SEC filing for the period ending January 26, 2025 attributes elevated data center revenue to accelerated computing and AI solutions, specifically citing Hopper architecture and Ethernet for AI. The disclosure also references customer advances and unearned revenue tied to hardware support, software, cloud services, and licensing, indicating a recurring-revenue layer alongside the core chip business.

Article language

English

Guidances Editorial Desk · Updated June 18, 2026 · Sources reviewed

Open article · no sign-in required

Sources and disclosure

Terms in this brief (3)

- market cap

- Share price × shares outstanding — the market’s total price tag on a company.

- capex

- Capital expenditure — money spent on long-lived assets like plants, equipment, or data centers.

- guidance

- A company's own forecast for its upcoming results.

What Happened

NVIDIA Corporation filed a periodic report with the U.S. Securities and Exchange Commission covering the fiscal period ending January 26, 2025. The filing, accessible via the SEC's EDGAR system, attributes higher data center revenue to demand for accelerated computing and AI solutions. Two product and infrastructure categories receive explicit mention: the Hopper GPU architecture and Ethernet for AI networking. The document also discloses customer advances and unearned revenue associated with hardware support contracts, software support, cloud services, and license arrangements, indicating a recurring-revenue layer alongside the company's core silicon business.

The source for this analysis is a search-provider snippet drawn from the SEC filing itself. The full text of the filing contains additional financial detail not available in the snippet; this analysis is therefore limited to the disclosed metadata and the factual context it supports.

Why the Market Cares

NVIDIA's data center segment has become the primary engine of the company's financial scale. With annual revenue of $215.9B and year-over-year revenue growth of +65.5%, the company's trajectory has been closely watched by technology investors, hyperscaler operators, and semiconductor supply-chain participants alike. A market capitalization of $4.96T places NVIDIA among the most valuable publicly traded companies globally, meaning that any shift in its disclosed revenue drivers can carry implications for index composition, institutional portfolio weights, and sector sentiment.

The explicit attribution of data center revenue growth to Hopper and Ethernet for AI is significant for several reasons. First, it indicates that the demand cycle driving NVIDIA's recent financial performance is not a single-product phenomenon but a platform story encompassing both compute silicon and the networking layer required to connect large GPU clusters. Second, the disclosure of customer advances and unearned revenue introduces a forward-looking dimension: these line items suggest that enterprise and hyperscaler customers are committing capital ahead of delivery, which can provide a degree of revenue visibility that pure spot-market chip sales would not.

For technology operators and AI infrastructure builders, the filing's framing supports the view that accelerated computing is now a baseline procurement category rather than an experimental budget line. The combination of Hopper-class GPU demand and Ethernet networking investment implies that customers are building out full-stack AI infrastructure, not merely acquiring isolated accelerators.

Technology and Policy Linkage

The Hopper architecture, NVIDIA's data center GPU generation preceding Blackwell, remains a central revenue contributor according to this filing. That detail matters for supply-chain and procurement planning: it indicates that the transition to next-generation silicon does not immediately displace prior-generation demand, a pattern consistent with enterprise upgrade cycles that tend to be staggered rather than simultaneous.

Ethernet for AI is a strategically important disclosure. The networking layer of AI infrastructure has become a competitive area, with NVIDIA's own InfiniBand historically important in high-performance computing clusters. The explicit mention of Ethernet for AI in a revenue-attribution context suggests that Ethernet-based AI networking—supported by NVIDIA's Spectrum-X platform—is gaining commercial traction. This has implications for the broader networking equipment sector and for hyperscalers evaluating open-standard versus proprietary interconnect strategies.

On the policy side, U.S. export controls on advanced semiconductors remain a material variable for NVIDIA's addressable market. The filing period predates several subsequent regulatory developments, but the data center revenue attribution to AI solutions is relevant to ongoing policy debates about compute access, national AI competitiveness, and the role of U.S. semiconductor companies in global AI infrastructure buildout. Operators and founders building on NVIDIA infrastructure may monitor export-control updates as a potential constraint on hardware availability in certain geographies.

The deferred revenue and customer advances disclosures also carry a policy dimension. As AI infrastructure spending becomes a subject of regulatory and competitive review in multiple jurisdictions, the structure of long-term customer commitments—whether through cloud service agreements, software licenses, or hardware support contracts—may attract additional disclosure review.

Market Lens

Trigger: NVIDIA's SEC filing for the period ending January 26, 2025, attributes data center revenue growth to Hopper GPU demand and Ethernet for AI, while disclosing a deferred-revenue base from support, software, cloud, and licensing arrangements.

Mechanism: Explicit revenue attribution in a regulatory filing provides a verifiable anchor for the AI infrastructure demand narrative. The deferred-revenue disclosure suggests forward revenue commitments from enterprise and hyperscaler customers, which affects near-term revenue predictability. Ethernet for AI revenue attribution broadens the investment thesis beyond GPU silicon to networking infrastructure.

Affected Sectors and Context: The semiconductor sector broadly, AI infrastructure operators, cloud hyperscalers, and networking equipment providers are the primary areas of relevance. NVIDIA's scale—$215.9B in annual revenue, +65.5% year-over-year growth, and a $4.96T market capitalization—means its disclosed demand drivers can serve as a reference point for adjacent sectors including memory, power infrastructure, and data center construction. This is market context only, not investment advice.

Time Horizon: The filing covers a period that has already closed. Its relevance is as a historical anchor for the demand cycle that has driven NVIDIA's recent financial performance. Forward-looking interpretation depends on whether Hopper demand has been sustained or superseded by Blackwell-generation products in subsequent quarters.

Next Check: NVIDIA's next earnings date is August 26, 2026, with consensus revenue estimated at approximately $91.7B for that quarter. That disclosure may indicate whether the Hopper-and-Ethernet demand narrative has evolved, whether Blackwell has fully displaced prior-generation revenue, and whether the deferred-revenue base has expanded or contracted. Operators and founders may also monitor any updates to U.S. export-control policy affecting advanced GPU shipments, as well as hyperscaler capex guidance from major cloud providers, which can function as a reference point for NVIDIA's data center order flow.

What to Watch Next

Several forward-looking indicators are worth tracking in the context of this filing:

Blackwell transition velocity. The filing covers a period when Hopper was the primary revenue driver. Subsequent quarters will reveal how quickly Blackwell-generation products have displaced Hopper in the revenue mix and whether the transition has created any demand gap or, conversely, increased total data center spending.

Deferred revenue trajectory. The disclosure of customer advances and unearned revenue is a relatively underanalyzed dimension of NVIDIA's business model. If this line item grows as a proportion of total revenue, it would indicate that NVIDIA is expanding a software and services layer with recurring-revenue characteristics—a structural shift distinct from the hardware cycle.

Ethernet for AI competitive dynamics. The explicit mention of Ethernet for AI as a revenue driver invites scrutiny of how NVIDIA's networking business is performing relative to InfiniBand and relative to third-party Ethernet switch vendors. Subsequent filings and earnings calls should provide additional granularity.

Export control developments. Any changes to U.S. Commerce Department rules governing advanced semiconductor exports will directly affect NVIDIA's addressable market for data center products. This is a policy variable with no fixed timeline but potential revenue implications.

Uncertainty and Constraints

This analysis is based on a search-provider snippet from the SEC filing, not the full document. Financial line items, segment breakdowns, and management commentary available in the complete filing are not accessible through the snippet alone. Readers requiring precise financial data should consult the full filing on SEC EDGAR directly. The market-data context used here is drawn from internal enrichment data and should not be treated as a substitute for official company disclosures or audited financial statements.

Market lens

On-device AI shifts attention from data-center chips to memory allocation and device margins

The useful read is whether local AI features create measurable pressure on memory mix, pricing, and product release schedules.

Impact path

Device AI → memory pressure

Signals to watch

- LPDDR and HBM allocation commentary

- AI PC and phone memory configurations

- Supplier lead times, spot pricing, and margin guidance

Verification schedule

D+1 · Jun 19

Do OEM launches raise baseline memory specs?

D+3 · Jun 21

Do suppliers change allocation or pricing language?

D+7 · Jun 25

Do device margins absorb or pass through memory cost?

Informational context only — not investment, legal, tax, or financial advice.

Builder Implications

- Infrastructure procurement planning: NVIDIA's explicit attribution of data center revenue to both Hopper compute and Ethernet networking indicates that full-stack AI infrastructure—not isolated GPU procurement—is a major enterprise buying pattern. Founders and operators building AI-native products may want to plan for integrated compute-plus-networking budgets rather than treating networking as a secondary consideration.

- Deferred revenue as a strategic signal: The disclosure of customer advances and unearned revenue tied to software, cloud, and licensing arrangements indicates that NVIDIA's enterprise customers are entering multi-period commitments. Builders evaluating NVIDIA's platform for long-term infrastructure may consider the contractual and support structures that accompany hardware procurement, as these affect total cost of ownership and vendor lock-in dynamics.

- Export-control risk management: The data center AI demand narrative documented in this filing is geographically sensitive. Founders and operators with international deployment requirements—particularly in markets subject to U.S. export controls—may maintain contingency plans for hardware availability constraints and monitor regulatory developments as an operational variable.

Want follow-up alerts? Subscribe by email after reading the public article.

Market lens

On-device AI shifts attention from data-center chips to memory allocation and device margins

The useful read is whether local AI features create measurable pressure on memory mix, pricing, and product release schedules.

Impact path

Device AI → memory pressure

Signals to watch

- LPDDR and HBM allocation commentary

- AI PC and phone memory configurations

- Supplier lead times, spot pricing, and margin guidance

Verification schedule

D+1 · Jun 19

Do OEM launches raise baseline memory specs?

D+3 · Jun 21

Do suppliers change allocation or pricing language?

D+7 · Jun 25

Do device margins absorb or pass through memory cost?

Informational context only — not investment, legal, tax, or financial advice.

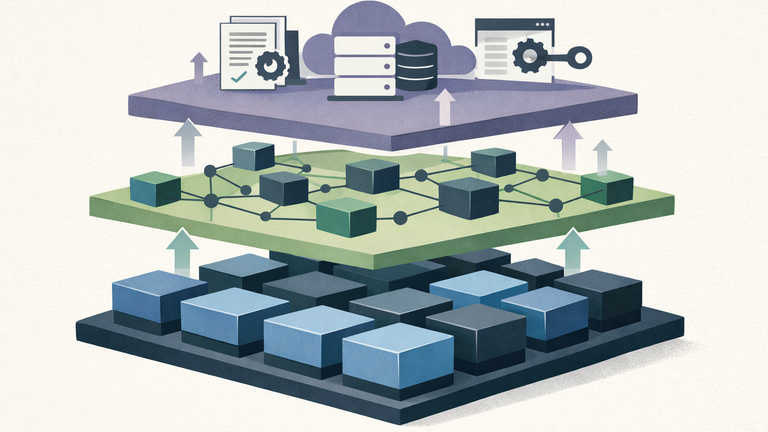

Visual Briefing

NVIDIA's SEC filing reveals a three-layer revenue model: compute (Hopper GPU), networking (Ethernet for AI), and services (support, software, cloud, licensing). Customer advances and unearned revenue indicate multi-period commitments, providing revenue visibility beyond spot-market chip sales.

Corrections and safety

See a factual, privacy, rights, or safety issue? Review the corrections process or contact Guidances before relying on this article for important decisions.